18 April 2024

Mastering CSRD Reporting Readiness

Antti Maunula

Partner & Co-founder

18 April 2024

Mastering CSRD Reporting Readiness

Antti Maunula

Partner & Co-founder

The CSRD poses extensive reporting requirements

The Corporate Sustainability Reporting Directive will start to apply gradually starting from January 2024. Initially, large companies with over 500 employees that are already subject to the Non-Financial Reporting Directive (NFRD) will start to report according to CSRD and the first reports are to be published in 2025. During the following years, the reporting scope will extend and will cover in total roughly 50 000 companies.

CSRD requires companies to disclose sustainability-related information in their financial reports. In total, the reporting directive includes around 1100 datapoints. However, the number of datapoints companies are expected to report on largely depends on the double materiality assessment carried out. In addition, some of the datapoints are voluntary and during the first two years companies with under 750 employees are provided phase-in options for some of the datapoints.

Implementing CSRD is a considerable challenge for all

Due to its extensiveness, responding to CSRD requirements is a considerable task for all companies and challenges are faced in implementation. Some of the key reasons for this are that:

Requirements are new for all and everybody is trying to figure out what needs to get done and how

During the past year, the regulation has been developing and more detailed guidelines still are

We don’t have many benchmarks available from practical application

Many organizations due not have experience in managing sustainability data in ways that would support efficient execution

Sustainability teams are short of resources to manage CSRD requirement fulfillment.

When companies embark on the CSRD journeys, there are many questions in the air. At the beginning of CSRD journeys, we hear questions related to double materiality assessment execution and discovering reporting requirements. Once these are clarified, companies start asking how to manage implementation efficiently, and during these journeys companies are wondering what is the expected outcome that will suffice.

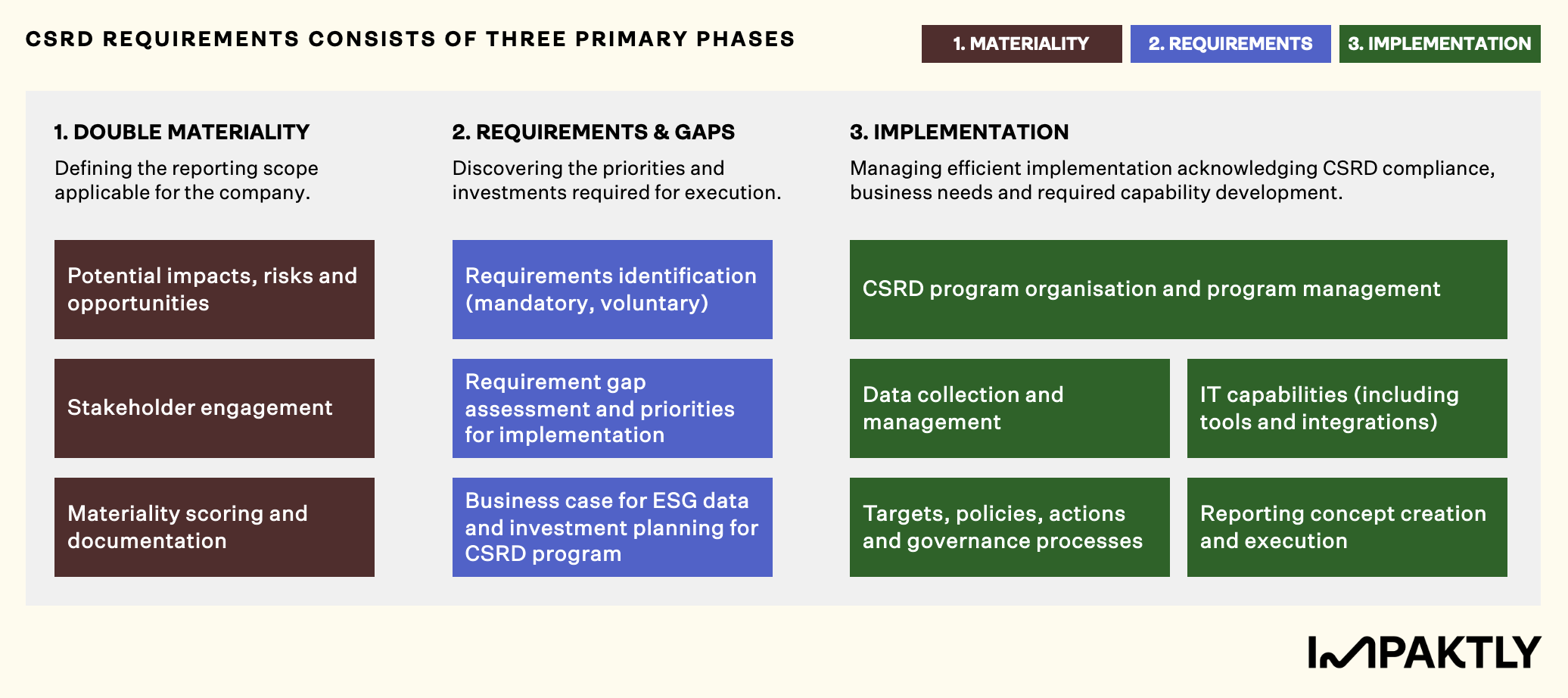

Responding to CSRD requires a structured approach

Responding to CSRD requirements consists of three primary phases:

Phase 1 - Double materiality: Defining the reporting scope applicable for the company.

Phase 2 – Requirements and gaps: Discovering the priorities and investments required for execution.

Phase 3 - Implementation: Managing efficient implementation acknowledging CSRD compliance, business needs and required capability development.

Phase 1: Double materiality assessment discovers sustainability priorities

The double materiality assessment is key in defining your reporting requirements. What’s more, the double materiality assessment is highly useful process to discover the key sustainability related priorities to generate business value. Through the double materiality assessment, you will identify the key negative impacts to minimize, business risks to mitigate and business opportunities to focus on.

Keep in mind the following when carrying out the assessment:

Aim for well-grounded definition of topics that are truly material

Focus on existing facts and industry insights in the evaluation and complement understanding through stakeholder engagement

Make a balanced evaluation of both impact and financial materiality, and ensure engagement with business, finance and risk teams for financial materiality assessment

Use the opportunity to discover the strategic significance of sustainability

Phase 2: Requirement definition is key for efficient execution

After the double materiality assessment, you are ready to start identifying concrete requirements for ensuring CSRD compliance. The mandatory requirements form the minimum scope for implementation. However, we recommend to also consider business requirements that can be met next to CSRD implementation.

Keep in mind the following when defining requirements for CSRD implementation:

Ensure holistic understanding of the reporting requirements

Evaluate gaps in datapoints and evaluate resources needed for execution

Identify business requirements that you prioritize in addition to compliance and build the business case

Get IT involved early to understand requirements and to jointly map to-be ESG data blueprint

Phase 3: Program organization is needed for successful implementation

Successful CSRD implementation requires coordination and broad organizational support. When setting up your program, it is important to ensure that you have a cross-functional steering group, adequate resources for program management, and roles and responsibilities are clear for your implementation streams.

Keep in mind the following in CSRD program implementation:

Ensure building a proper program organisation, which includes engagement with key functions

Build adequate support for program streams and highlight barriers and deviations early

Drive IT capabilities considering the role of sustainability for the business and existing IT landscape

Ensure changes in business processes are adopted – remember the importance of communications and training

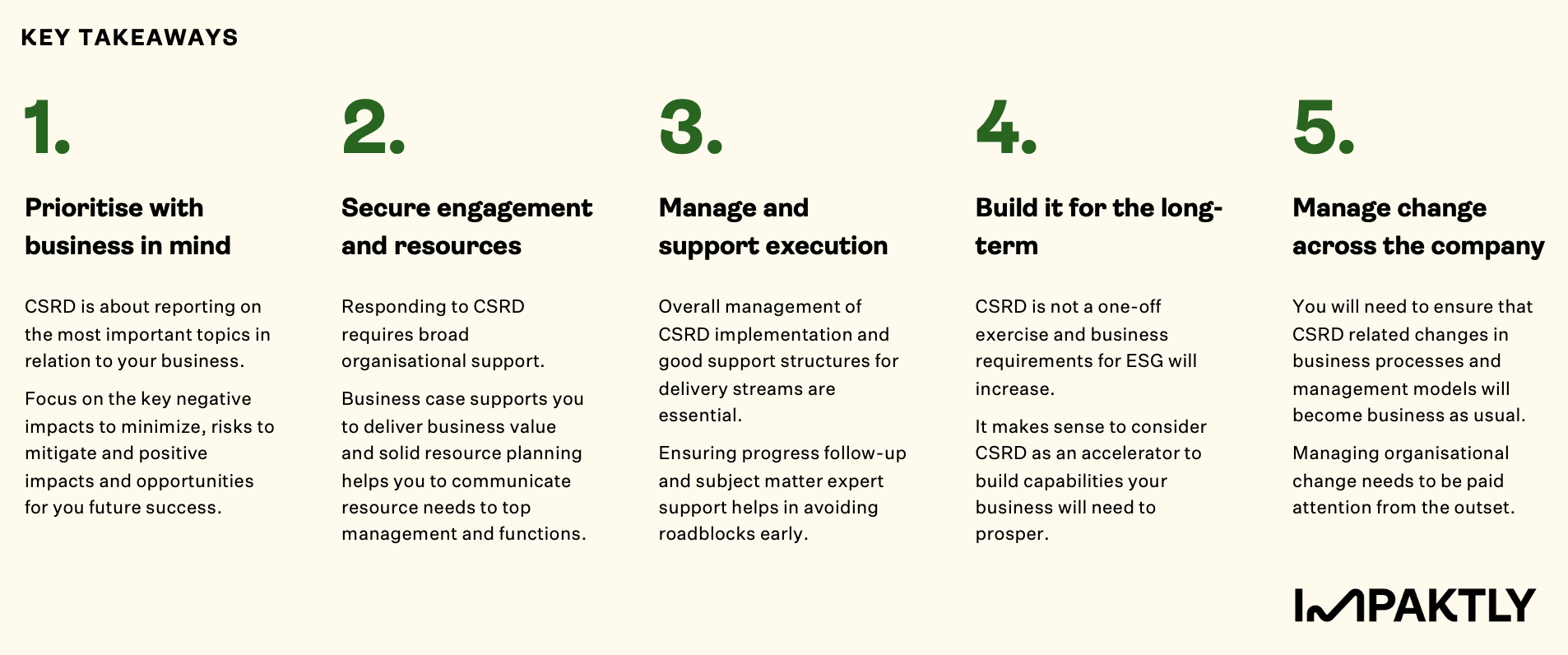

Key takeaways for your CSRD implementation journey

CSRD requires a fair amount of work and to be able to respond to the requirements efficiently, a good amount of time should be used to prioritization. When planning your CSRD program it is important to ensure, you have the organization onboard – top management commitment, support from key functions and resources reserved for execution. Build your program management structure enabling holistic coordination and dividing work in streams. Remember that CSRD is not a one-off exercise and in addition to regulation, stakeholder requirements for sustainability will increase. Try to do things in a smart way and way that will benefit for your business in the long-term. Finally, CSRD will require you to adapt your business processes and it is important to drive change alongside requirement execution.

Let's talk about how to make this happen!

Curious what this could mean for your team? Get in touch, we'd love to chat.

Mia Folkesson

Managing Partner

mia@impaktly.com

Let's talk about how to make this happen!

Curious what this could mean for your team? Get in touch, we'd love to chat.

Mia Folkesson

Managing Partner

mia@impaktly.com